Key aspects of RDL 13/2022, of July 26, new contribution system for self-employed workers and CATA improvement

Royal Decree-Law 13/2022, of July 26, which establishes a new contribution system for self-employed or self-employed workers and improves protection for termination of employment activity

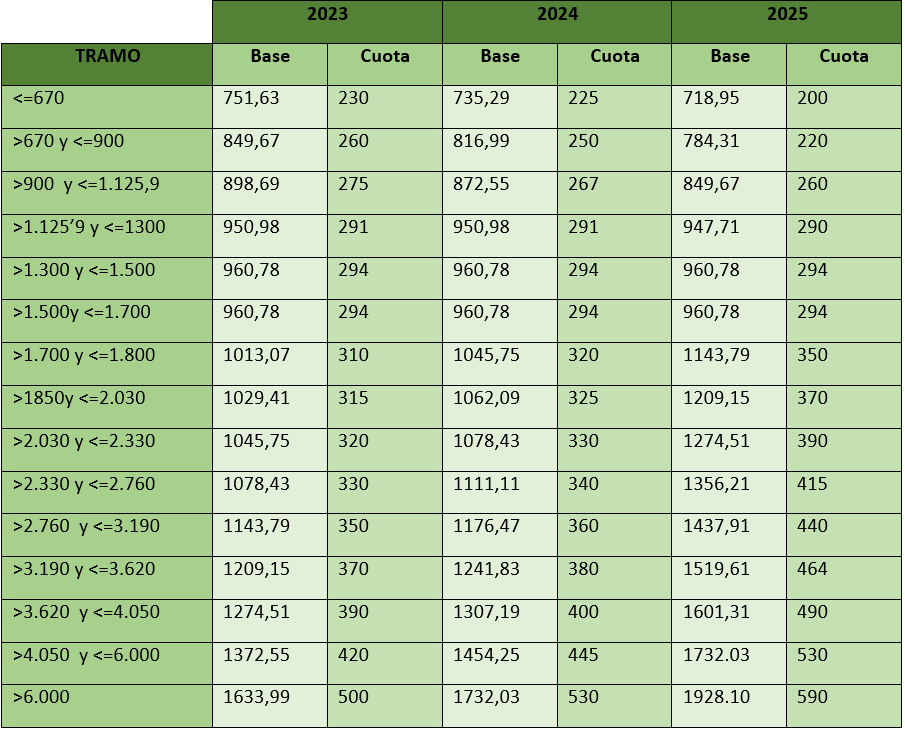

This reform establishes, for the next three years, a system of fifteen sections that determines the contribution bases and quotas based on the net income of the self-employed worker.

This standard will come into force as of January 1, 2023 and will continue to be implemented gradually over a maximum period of 9 years, with periodic reviews of three years, with the implementation period initially agreed between the years 2023 and 2025.

The decree defines the concept of net income, which must be calculated by deducting from the income all the expenses that have been generated during the exercise of the activity and that are necessary to obtain income for the worker. autonomous.

___Monthly contributions of Social Security for self-employed people with low incomes are You will see reduced by 30% compared to the current one. Self-employed workers with earnings lower than the minimum interprofessional wage will have the option of choosing a contribution base within a reduced table provided for them.

In any case, the bases chosen will have provisional nature, until they are regularized based on performance annual results obtained and communicated by the corresponding Tax Administration starting from the following financial year with respect to each self-employed person.

Once the corresponding fiscal year has ended and the final annual net returns are known, the actual contributions will be regularized and quotas may be claimed or returned to the TGSS in the event that the returns do not correspond with the forecasts that have been made during the year. In the event that once the regularization has been submitted, the self-employed person has the right to the refund, the TGSS will be the one to regularize it ex officio before April 30 of the year following the one in which the corresponding Tax Administration has communicated the computable income to the General Treasury of Social Security.

On the contrary, if the provisional contribution made is lower than the quota corresponding to the minimum contribution base of the section in which their income is included: the self-employed person must enter the difference between both contributions until the last day of the month following that in which they are included. notify the result of the regularization, without application of late payment interest or any surcharge to be paid within that period.

___As for the protection improvements, the modalities of the cessation of activity are expanded to improve coverage of different contingencies, and the protection provided to salaried workers by the RED mechanism established in the labor reform is adapted to self-employed workers.

Self-employed workers who, as of January 1, 2023, are registered with the RETA (or the RETM) must communicate by media electronic to the General Treasury of Social Security, before October 31, 2023, the data related to paragraphs 1 to 8 of article 30.2.b) of the General Regulation on company registration and affiliation, registrations, cancellations and variations of worker data in the Security Social.

Another novelty that we find in this RDL is the elimination of the current restrictions associated with the age for the contribution of people who are registered with the RETA. With this new model, self-employed people aged 47 or over will be able to increase their contribution base in the last stage of their working life as long as their income increases.

News that will begin to be applied on January 1, 2023:

|

Establish contribution tables based on the returns obtained during the years 2023, 2024 and 2025. The workers included in the RETA must contribute based on the full returns obtained. |

|

___Possibility of making up to six annual changes to the contribution base.This option can be used in the event that during the current fiscal year the income obtained by the self-employed worker varies. ___ |

|

___Adapt the bonuses and reductions in the contribution to the Special Regime for Self-Employed Workers to the contribution for sections___HT MLTAG242___.___ |

|

Implementation of a reduced fee of 80 euros per month between the years 2023 and 2025 for the start of a self-employed activity, or in cases where that the self-employed person had not been registered in the two years immediately preceding the effects of registration. ___This measure will apply during the first 12 months, and may be extended for a further 12 months in the event that the returns obtained during the first year are lower than the Minimum Interprofessional Wage. The reduced fee will be maintained until the end of the first twenty-four full calendar months, and 160 euros from the month twenty-fifth |

Quote sections available (fifteen):