Review of extraordinary benefits for cessation of activity regulated in art. 17 of Royal Decree-Law 8/2020, of March 17

In March 2020, several urgent and extraordinary measures came into force to address the economic and social impact of COVID-19, including an extraordinary cessation of activity benefit (hereinafter, PECATA) intended for self-employed workers who were forced to suspend their activity due to the declaration of the state of alarm, or who had experienced a reduction in their turnover of at least one 75% in relation to the average billing of the previous calendar semester.

Due to the urgency and need to deliver these benefits to the homes of the workers who needed them, a provisional recognition of them was carried out, making the final recognition subject to a subsequent review by the Mutual Funds Collaborating with Social Security.

Once all preventive measures related to the health crisis situation derived from COVID-19 have been completed, at Fraternidad-Muprespa we have begun the review of the PECATA that were provisionally recognized.

The review of the PECATA is being carried out by verifying two scenarios: on the one hand, compliance with the access requirements and, on the other, verification of the amounts paid. If any incident has arisen during these verifications, we will have sent you a letter with the subject: “hearing procedure” in which we detail the incidents detected and give you a period of 15 business days (that is, not counting Saturdays, Sundays or holidays) to be able to make allegations or provide documentation that will clarify or correct the incident detected.

The recommended channel to respond to the hearing procedure: These resolutions may be of three types:

a) Resolution that elevates the provisional agreement to final: will be issued when the doubts have been clarified during the review, no incident is detected and it is declared that the benefits paid have been correct.

b) Resolution that annuls the provisional agreement: will be issued when during the review incidents have been detected that prevent access to the benefit and that have not been corrected or documented documentaryly during the processing process. audience. In these cases, the benefits paid will be declared as unduly received and will be claimed.

c) Resolution that modifies the provisional agreement: will be issued when during the review compliance with the requirements to access the benefit has been verified, but incidents have been detected in the total amount of the benefit paid and during the hearing process these have not been clarified differences. In these cases the right to access the benefit will be recognized, but the differences in the excess of the benefits paid will be claimed.

FREQUENTLY ASKED QUESTIONS

1. How to process allegations?

Any means of notification will be admitted to present the allegations that it deems appropriate. However, at

The allegations received by this means will provide you with immediate acknowledgment of receipt and the possibility of online monitoring of the processing status. Furthermore, allegations received by this means will be resolved on a preferential basis.

However, you can also send us your allegations by any other means (recommending that it be a means that reliably accredits delivery).

Consult the address of your nearest management center: Fraternidad.com/centros .

If you are the advisor of the self-employed worker and you have a Digital Office user, we recommend that you complete the allegations process by accessing the following link: Fraternidad.com/oficinadigital

En cualquier otro caso, si aún no dispone de usuario de Oficina Digital, podrá realizar el trámite de alegaciones a través de la siguiente dirección: href="/download/manual-officina-digital-servicio-de-respuesta-tramite-de-audiencia-cata-covid" target="_blank"> manual .

2. Incidents related to access to the benefit

During the review the following points will be analyzed:

a) Being registered in the Special Regime of the Social Security at the time the PECATA accrual begins and, in any case, prior to March 14, 2020.

b) Be up to date with the contributions with Social Security at the time the PECATA accrual begins.

c) That the activity carried out (according to the CNAE) is framed within one of the assumptions of access to the benefit . That is, the activity is among those expressly suspended due to the declaration of the state of alarm or among those that are understood to demonstrate a reduction in turnover, at least 75% in relation to the average turnover of the previous calendar semester (since the TGSS has indicated that they meet the criterion that the average daily number of active workers affiliated with the Social Security system in that CNAE, expressed at four digits, during the period to which the benefit corresponds, is more than 7.5% lower than the average daily number corresponding to the second half of 2019).

It should begin by clarifying that affiliation to Social Security is the responsibility of the General Treasury of Social Security (TGSS) and that the Mutual Fund can only access to verify the information, but cannot modify it.

Within the verification acts in the review of the PECATA, the Mutual Fund has agreed to verify the affiliation status that, today, appears in TGSS for the date of access to the benefit. It could be that since you requested the benefit there has been some modification in your affiliation that affected the provisional recognition that was given to you.

In these cases, you must request a certificate from the TGSS indicating that as of 03/14/2020 you were registered in the Special Regime and that said registration has not been subsequently revoked. Alternatively, it would be enough for the TGSS to regularize the information in its database and the Mutual Fund would agree to verify it directly.

In any case, you can always provide any documentation admitted by law that you consider can prove the registration requirement in the Special Regime.

First of all, we must indicate that the debt information has been obtained from the databases of the General Treasury of Social Security (TGSS) and that the Mutual Fund only has consultation access to said data, and cannot clarify or modify said information.

To prove the non-existence of the debt there are the following alternatives:

- Provide a certificate from the TGSS that proves that on 03/14/2020 you were up to date with all debts with Social Security.

- Provide a resolution from the TGSS to defer the debt you may have as of 03/14/2020. Said resolution must be prior to 03/14/2020 and be accompanied by documentation that proves having complied, in the period 03/14/2020 to 06/30/2020, with the amortization periods indicated in the aforementioned resolution.

- If during the receipt of the PECATA you received an invitation to pay the fees owed, you may provide documentation that justifies that you were up to date with said fees within 30 days of receipt.

Otherwise, this invitation will have been made along with the hearing process and, therefore, you will have 30 calendar days to pay all the debt, prior to 03/14/2020, that you owed with Social Security. If you pay said debt, you must provide proof of payment of the debt and a certificate from the TGSS that you are up to date with payment as of 03/14/2020.

Important: For the purposes of catching up on payment of the debt prior to 03/14/2020, the recognition of a debt deferral after said date will have no effect (only the effective payment of the debt will have that effect).

In any case, you can always provide any legally accepted documentation that you consider can prove that you were up to date with your Social Security contributions.

When in the hearing process it is indicated that the reason for request is not sufficiently justified, it means that:

a) If you requested the benefit due to suspension of your activity:

In this case, during the review of your benefit it has been observed that the National Code of Economic Activities (CNAE) of the activity in which you were registered in the General Treasury of Social Security (TGSS) was not included within of those who have been considered obliged to suspend the activity (whether due to state, regional or local regulations).

You may justify access to the benefit by providing the rule that you consider prevented you from continuing with your activity, expressly indicating the specific section that you consider was applicable to you. In this case, along with the documentation, we recommend that you explain in your own words the reasons that you consider forced you to suspend your activity.

Please note that the voluntary suspension of the activity is not a reason to access the benefit through this means , if this is the case we recommend that in the allegations you consider requesting access by means of billing reduction.

b) If you requested the benefit for reduction of your billing:

In this case, during the review of your benefit it has been observed that the National Code of Economic Activities (CNAE) of the activity in which you were registered in the General Treasury of Social Security was not included among those are presumed to comply with said reduction (activities that experienced a reduction of more than 7.5% in the average daily number of active workers affiliated with the Social Security system, during the period of receipt of the benefit, in relation to the second half of 2019 - Second additional provision of Royal Decree-Law 3/2021, of February 2-).

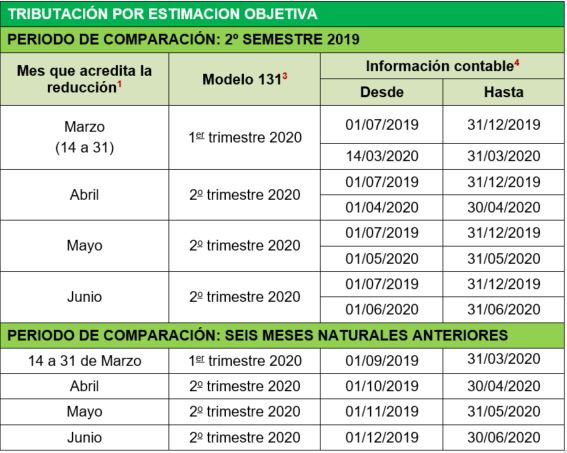

Consequently, in the hearing process, you must indicate the month in which the reduction of at least 75% is accredited, in relation to the average of the previous six calendar months* and provide the tax and accounting documentation that allows such verification.

(*) Clarifications to the comparison period of the previous 6 calendar months indicated by the standard:

1) The General Directorate of Social Security Regulation has established a criterion which indicates that the self-employed may choose the period that most favors them from the following options: the last semester of 2019 (July – December) or the six calendar months prior to the month in which they must prove the billing reduction.

2) Those self-employed who have registered in the special regime after July 1, 2019, will not be able to compare with the second half of 2019 and will necessarily have to do so with the 6 calendar months prior to the reduction. Additionally, those who had not been registered in the previous 6 calendar months will be compared only with the monthly average of the months in which they had been registered (prior to the reduction).

3) The month in which the reduction in billing is accredited will not necessarily have to be the one prior to the date of submission of the application, but rather the month in which the self-employed person can actually prove the reduction in billing.

4) For the self-employed in certain artistic activities and the campaign period in seasonal agricultural and fishing activities, the monthly average from March 2019 to February 2020 will be taken into account.

You can justify access to the benefit by providing the following form:

This form, depending on the modality of taxation, of the month in which the billing reduction is accredited and the comparison period chosen to contrast it, must be accompanied by the following documentation:

1 Month in which the billing reduction required in the norm. Normally it will coincide with the month of the benefit's effects, but if you cannot prove the reduction in said month, but can prove it in one of the subsequent months, you may indicate the month in which the requirements meet.

2 Those self-employed persons who are exempt from submitting VAT should not provide these models.

3 Companies should not provide these models. Instead, they must provide documentation that proves their connection with the company (partner's book or registered shares registered in the commercial registry, company deeds or any means of proof admitted by law).

4 The accounting information presented must reflect the billing subtotals for each of the months indicated in the period.

If the month in which the billing reduction is credited was March 2020, it must be subdivided into two subtotals, the one corresponding to billing between March 1 and 13 and the one corresponding to billing between March 14 and 31.

Although any means of proof admitted by law may be presented as accounting information (record book of invoices issued and received; daily book of income and expenses; record book of sales and income, etc.), it is recommended to provide this accounting information in the Excel model attached to the sworn declaration.

5 In Provincial Territories all VAT returns for the year and the annual form 390 must be provided.

Alternatively to the previous methods, you may also justify access to the benefit through the following options:

- Alleging and documenting that the activity that was carried out and justified its inclusion in the Special Regime was different from the one that the Mutual Fund has evaluated in your review.

In this case, you must regularize your situation in the TGSS and provide the following documentation:- TGSS document that certifies the new activity and that covers the period 03/14/2020 to 06/30/2020.

- Economic activities tax for the year 2020.

- Any other document admitted by law that accredits or endorses the exercise of the activity that is intended to be alleged.

- Requesting in the allegations a NOVATION in the reason for requesting the benefit. That is, if you requested the benefit for “Suspension” and your activity was not among those that were forced to suspend the activity due to the requirement of a rule, you may request that your request be evaluated for “Reduction” of billing, and vice versa. In both cases, along with this novation request, you must provide documentation that proves access for the new reason.

Please note that the scope of the benefit due to “Reduction” is somewhat smaller than due to “Suspension”, since the start date of the benefit will not always be 03/14/2020 (it will depend on the date on which the benefit was requested and the month in which the reduction in billing is verified) nor will it always end on 06/30/2020 (since if caused withdrawal from the special regime before said date, the benefit would be extinguished on said day). It is important to take into account this difference because although the novation may facilitate access to the benefit and the total amounts paid may no longer be claimed, it could be that a part of it may still have to be claimed (for the reasons already explained).

3. Incidents related to the amount of the benefit received

There are several reasons that may result in a higher benefit being paid than what should have been due. Among them, the most common are the following:

a) Overlapping with other Social Security benefits: the PECATA benefit is not compatible with the receipt of other Social Security benefits that, in turn, were not compatible with the development of self-employed activity. If during the receipt of PECATA you also benefited from other Social Security benefits (temporary disability, birth and care of a minor - former maternity/paternity -, risk during pregnancy or breastfeeding, permanent disability, retirement,...) the days in which both benefits coincided simultaneously will be deducted and claimed from the PECATA benefit.

b) Difference in the type of benefit paid: PECATA had two types of protection: benefit (for those people who had contributed 12 or more monthly payments to the Cessation of Activity coverage immediately prior to 03/14/2020) and subsidy (for those who do not have those 12 monthly payments). Due to the difficulties in accessing information in the first period of the pandemic, PECATAs could be recognized in a different way than what would have really corresponded. If that were the case, during the review, a recalculation would have been carried out according to the correct modality and any differences that may exist would have been claimed.

c) Differences in the regulatory basis. Due to the difficulties in accessing information in the first period of the pandemic, PECATAs could be recognized with a higher regulatory basis than what would have really corresponded. If this difference had been detected during the review, the benefit would have been recalculated in accordance with the correct regulatory basis and any differences that may exist would have been claimed.

d) Differences in the days of benefits paid. If during the review it was detected that the benefit was paid for more days than would have been due, the benefit would be recalculated and the differences would be claimed. The differences in days of benefit payment may be due to overlapping periods with other benefits, to benefits recognized for "reduction in billing" that had been paid after the date of withdrawal from the special regime (when this had occurred prior to 06/30/2020) or that had been recognized prior to the date that would have corresponded based on the presentation date and/or the month in which the reduction in billing was credited.

When in the hearing process it is indicated that incidents have been detected on the start date of the benefit, it means that during the PECATA review it has been determined that the payment of the benefit began on a date earlier than what should have corresponded (based on the information in the file).

The start date of PECATA depended on several factors:

- The reason for the request: suspension of activity or reduction in billing.

- The date of entry into force of the rule that required the suspension of the activity.

- The month in which the billing reduction was credited.

- The date of submission of the application.

- The termination of Social Security benefits that you may be receiving when the right to PECATA is provisionally recognized and that is incompatible with the exercise of self-employment.

In the event that the reason for requesting PECATA had been the suspension of the activity, the start date of the benefit will be the date of entry into force of the rule that expressly prevents continuing with its activity. As a general rule, this date will be March 14, 2020, for most of the activities that were suspended due to the declaration of the state of alarm; but it could be that its activity was expressly suspended by a later publication rule, such as activities related to hairdressing or tourist rentals or others that were regulated in regional or local regulations.

On the contrary, if the reason for the PECATA request had been a reduction in billing, the start date of the benefit would coincide with the first day of the month in which the aforementioned reduction in billing is credited, unless the losses are credited in the month of March, in which case the benefit would accrue from the 03/14/2020. In this sense, the rule provides that the month in which the reduction is credited is the month immediately preceding the month in which the application was submitted (except for applications submitted in the month of March itself, which are understood to refer to the same month).

You may justify access to the benefit from a date other than that calculated by the Mutual Fund in the PECATA review, providing the following documentation:

- If you requested the benefit for “ suspension of activity ”: may provide the regulations (state, regional or local) that expressly prevented it from continuing to develop its activity. You may also provide any documentation admitted by law that proves the manifest impossibility or force majeure, unrelated to the regulations stated above, that prevented you from continuing your activity. In the latter case, the documentation provided must expressly state the date from which said forced suspension occurred.

- If you requested the benefit for “billing reduction ”: you may allege the reasons why you understand that there is an error in the month in which the Mutual Fund has valued the billing reduction. For example, providing proof of submission of the application. ( see FAQ 2.4.b ).

When in the hearing process it is indicated that incidents have been detected on the end date of the benefit, it means that during the PECATA review it has been determined that the payment of the benefit was finalized on a later date than it should have corresponded (based on the information in the file).

The main causes that may lead to differences in the end date of the benefit are the following:

- Having requested the PECATA for “ reduction in billing ” and having canceled the special regime before 06/30/2020 and that the Mutual Fund had continued paying the benefit after said cancellation date.

- Having been a beneficiary of another Social Security benefit -incompatible with self-employment- until 06/30/2020 or beyond and having simultaneously received the PECATA.

You may justify access to the benefit until a date other than that calculated by the Mutual Fund in the PECATA review, providing any documentation admitted by law that refutes the facts previously stated, such as:

- Updated work life report, or TGSS certificate, stating that you did not leave the special Social Security regime in the period 03/14/2020 to 06/30/2020.

- Certificate from the INSS stating that they have not received Social Security benefits incompatible with self-employment in the period 03/14/2020 to 06/30/2020.

If in the hearing process it has been indicated that possible overlaps in Social Security benefits have been detected, it is because the information provided to the Mutual Insurance Companies by the National Social Security Institute (INSS) has detected that they have been a beneficiary of some other Social Security benefit incompatible with self-employment.

Given that the Mutual Fund cannot autonomously verify this information, to refute it, you must provide along with your allegations a certificate issued by the INSS reporting the Social Security benefits that you may have received in the period 03/14/2020. 06/30/2020 clearly indicating: type of benefit, start date and end date.

In the event that you have not been a beneficiary of any benefit, you must provide a certificate from the INSS that expressly indicates that you have not received any Social Security benefit in the period 03/14/2020 to 06/30/2020 (except, obviously, PECATA).

If you belong to the Special Regime of the Sea, in any case, a certificate from the Social Institute of the Navy will be necessary in which it is expressly indicated that you were not a beneficiary of aid for fleet paralysis in the period 03/14/2020 to 06/30/2020 or, if you received them, the exact dates on which you received them (start and end of aid).

When in the hearing process it is indicated that it has been detected that the benefit was paid for an amount greater than the amount that would have corresponded to you, it means that during the PECATA review it has been determined that errors occurred in the calculation of the daily amount that was established for your benefit or in the days on which benefits were paid, in both cases the conclusion is that the benefit was paid for an amount greater than that which would have corresponded to you.

In order to review your benefit again, you must provide, along with your allegations, the following documentation and information:

- Documentation proving that you have been contributing for the contingency of cessation of activity during the 12 months prior to the declaration of the state of alarm (12 months prior to 03/14/2020): among others, it may be a certificate from the TGSS or a copy of the contribution charges made by the TGSS in the aforementioned period.

- Certificate of contribution bases issued by the General Security Treasury, which includes the 18 months prior to July 2020 (or the months in which you were registered in the special regime).

- Family book, to verify the number of dependent children.

- Economic Activities Tax for the year 2020, to verify the activity carried out.

4. Doubts after exceeding the deadline for the hearing process

Once the deadline granted in the hearing process has passed, the Mutual Fund will proceed to issue a final resolution evaluating the allegations and/or additional documentation that it may have received.

With the information in the file, it will issue one of the following final resolutions:

a) Resolution that elevate the provisional agreement to final: it will be issued when the allegations and/or documentation provided have allowed the detected incidents to be resolved favorably. In this case, access to the benefit and also the amounts paid will be declared correct.

b) Resolution that annuls the provisional agreement: if despite the allegations and/or documentation provided they do not allow clarification of the incidents that prevented recognition of access to the benefit and, therefore, to the amounts perceived. In these cases, a resolution will be issued that revokes the provisional agreement, declares the amounts paid as undue benefits and claims said amounts in their entirety.

c) Resolution that modifies the provisional agreement: will be issued when the allegations and/or documentation provided have made it possible to resolve the incidents that could prevent access to the benefit, but were not sufficient to determine that the total amount paid was correct. In these cases, a favorable resolution will be issued in relation to the right of access to the benefit, but it will declare that part of the benefits paid were improper, proceeding to claim the amounts paid in excess.

As informed at the end of the resolution that has been sent to you, if you are not satisfied with said resolution, you may file a prior claim through judicial channels.

The period to submit the prior claim is 30 business days (that is, excluding Saturdays, Sundays and holidays) counted from the date on which you received the resolution.

Given that this prior claim is mandatory for the initiation of subsequent judicial proceedings, we recommend that you present it by some means that reliably accredits its delivery.

Once the deadline granted in the hearing process has passed, the Mutual Fund has no obligation to analyze the allegations or documentation received. However, if your file has not yet been resolved, the Mutual Fund, in order to resolve it with as much information as possible, will analyze the documentation received (even after the deadline).

On the contrary, if the Mutual Fund receives your allegations and/or documentation once the resolution has been issued, if this is contrary to your interests, you must present a prior claim (in which you may incorporate the allegations and/or documentation that the mutual company could not assess when issuing the resolution).

5. Examples of how to fill out the allegations form to prove the reduction in billing

Assuming that you received the benefit with effect from April 1, 2020, you must fill out this form following the following guidelines:

- In section (A) you must record the billing in each of the months included in the quarter of the month in which credit the billing reduction (April, May and June) and you must exclusively check the box for the month of April.

- In section (B) you must enter the billing for all the months in the table in which you have been registered in the Special Regime and you must choose the criterion with which you want the reduction in billing to be calculated (comparing the month of April with the second half of 2019 or with the 6 calendar months and prior to April 2020). Assuming that the most favorable period (the one with the highest billing volume) was the 2nd semester of 2019, this option would be marked.

The documentation that should be provided along with the sworn statement would be the following:

- Copy of form 303 for the 3rd and 4th quarters of 2019 + 2nd of 2020.

- Copy of model 130 of the quarters: 2nd, 3rd and 4th of 2019 + the 1st and 2nd of 2020.

- Accounting documentation that justifies the billing for the months July to December 2019 and the months of April, May and June 2020 (preferably using the Excel provided with the form, although any other document accepted by law is acceptable).

Finally, you must keep and make available to Fraternidad-Muprespa the originals of the income or sales invoices that justify the amounts recorded.

Assuming that you received the benefit with effect from March 14, 2020, you must fill out this form following the following guidelines:

- In section (A) you must record the billing in each of the months included in the quarter of the month in that certifies the reduction in billing (January, February and the two periods of March) and must exclusively mark the box for the month of the March period (14 to 31).

- In section (B) you must enter the billing for all the months in the table in which you have been registered in the Special Regime and you must choose the criterion with which you want the reduction in billing to be calculated (comparing the period from March 14 to 31 with the second half of 2019 or with the 6 calendar months prior to the chosen month). Assuming that the most favorable period (the one with the highest billing volume) was the previous 6 calendar months, this option would be marked.

The documentation that should be provided along with the sworn statement would be the following:

- Copy of form 131 of 1 er quarter of 2020.

- Accounting documentation that justifies the billing for the period from September 1, 2019 to March 31, 2020 (differentiating in the month of March the billing from 1 to 13 from that corresponding to 14 to 31). In this sense, it is recommended to provide the Excel provided with the form, although any other document accepted by law would be admissible.

Finally, you must keep and make available to Fraternidad-Muprespa the originals of the income or sales invoices that justify the amounts recorded.